London

Roots Analysis has announced the addition of the “Biopharmaceutical Contract Manufacturing Market, 2022–2035” report to its list of offerings.

In pursuit of both time and cost savings, as well as to access higher scales of production, outsourcing has emerged as a lucrative option for biologic drug developers. Driven by several blockbuster products, a burgeoning pipeline of biologic drugs, the demand for reliable contract service providers, which have the required expertise and advanced manufacturing capabilities, is expected to grow at a commendable pace in the coming years. Currently over 275 companies claim to be biopharma CDMO / biopharma CMO, in compliance with the regulatory standards. It is also worth highlighting that biopharmaceutical contract manufacturers are actively trying to consolidate their presence in this field by entering into strategic alliances in order to meet the indubitably rising demand for biologics. In 2021, a sum of over USD 70 billion was invested in the cell and gene therapy domain. However, biologics manufacturing is fraught with various challenges.

Key Market Insights

Presently, more than 275 players offer contract manufacturing services for biologics

This segment of the industry is dominated by the presence of mid-sized players (51-200 employees) and start-ups / small players (2-50 employees), which collectively represent more than 80% of the total contract manufacturers. In addition, it is important to mention that about 33% of the firms were founded post 2010.

Approximately 60% of the players carry out manufacturing operations across all scales of operation

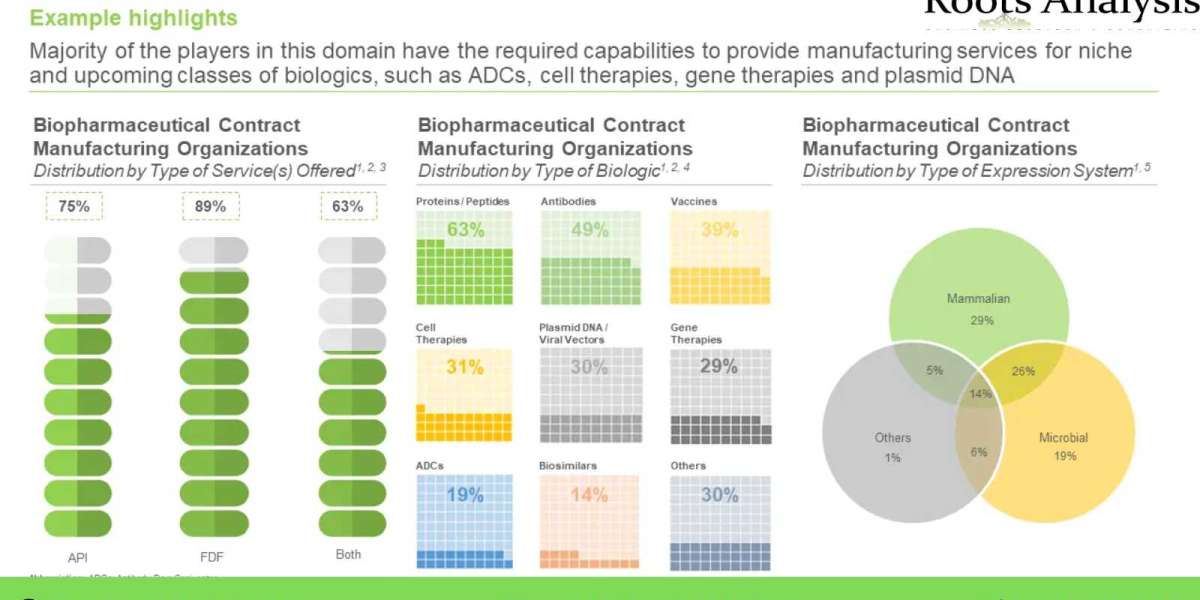

More than 60% of the service providers are engaged in manufacturing of recombinant proteins and peptides. This was followed by 49% CMOs that claim to have the required capabilities to provide antibody manufacturing services. It is worth mentioning that a number of biologic manufacturers in this domain have the required capabilities to provide manufacturing services for niche and upcoming classes of biologics, such as ADCs, cell therapies, gene therapies and plasmid DNA.

450+ manufacturing facilities dedicated to biologic-based therapies have been established globally

North America has emerged as a key manufacturing hub for biotherapeutics, featuring the presence of nearly 33% of the total manufacturing facilities. This is followed by facilities located in Europe and Asia-Pacific. Prominent manufacturing hubs within Europe include (in decreasing order of number of facilities) Germany, the UK, France, Italy and Spain.

800 partnerships were established in this domain, during the period 2015-2022

Partnership activity of biologic contract manufacturers has increased at a CAGR of 42%, during the given period. Manufacturing agreements emerged as the most popular type of partnership model adopted by industry stakeholders (37%), followed by product development and manufacturing agreements (19%). Further, over 80% of the expansion projects undertaken by industry stakeholders were initiated since 2020.

Expansion activity in this domain has grown at a CAGR of 49%, during the period 2016-2022

More than 45% of such initiatives were focused on establishing new facilities, followed by those undertaken for expanding the existing facilities (23%). It is worth mentioning that most of expansion initiatives were carried out for gene therapies (29%), followed by those focused on cell therapies (28%) and vaccines (20%).

Currently, 54% of the overall, installed biopharmaceutical contract manufacturing capacity is for mammalian expression systems

The maximum (49%) capacity is installed with players companies based in Asia-Pacific. It is worth mentioning that the aforementioned region has a higher number of players engaged in biopharmaceutical contract manufacturing, which have further established multiple production facilities. This is followed by the capacity available with players having headquarters in North America (25%) and Europe (24%).

Europe and Asia-Pacific are anticipated to capture over 70% of the market share, in 2035

In terms of type of service(s) offered, the current market is driven by APIs (close to 56%); this trend is unlikely to change in the foreseen future. Further, based on scale of operation, majority of the revenue share (87%) of the overall market in 2035 is projected to be driven by commercial operations.

To request a sample copy / brochure of this report, please visit this

https://www.rootsanalysis.com/reports/250/request-sample.html

Key Questions Answered

- Who are the key players engaged in offering contract manufacturing services for biopharmaceuticals?

- What are the different partnerships and expansion initiatives undertaken by biopharmaceutical contract manufacturers in the recent past?

- Which regions represent the current key contract manufacturing hubs for biopharmaceuticals?

- What is the current, installed capacity for contract manufacturing of biopharmaceuticals?

- What is the current, global demand for biologics? How is the demand for such candidates likely to evolve in the foreseen future?

- What percentage of the biopharmaceutical manufacturing operations are presently outsourced?

- What factors should be taken into consideration while deciding whether the manufacturing operations for biopharmaceuticals should be kept in-house or outsourced?

- How is the current and future opportunity likely to be distributed across key market segments?

The financial opportunity within the live biotherapeutic products and microbiome contract manufacturing market has been analyzed across the following segments:

- Type of Service(s) Offered

- API

- FDF

- Type of Biologic Manufactured

- Antibodies

- Cell Therapies

- Vaccines

- Other Biologics

- Type of Expression System Used

- Mammalian

- Microbial

- Others

- Scale of Operation

- Preclinical / Clinical

- Commercial

- Company Size

- Small

- Mid-sized

- Large and Very Large

- Key Geographical Regions

- North America

- Europe

- Asia-Pacific

- Latin America

- MENA

The report includes profiles of key players (inexhaustive list provided below); each profile features an overview of the company, details related to its service portfolio, facilities dedicated to biologic manufacturing, recent developments and an informed future outlook.

- AGC Biologics

- Catalent

- Cytiva

- FUJIFILM Diosynth Biotechnologies

- KBI Biopharma

- Patheon

- Piramal Pharma Solutions

For additional details, please visit

You may also be interested in the following titles:

- Peptide Therapeutics: Contract API Manufacturing Market: Industry Trends and Global Forecasts, 2022-2035

- Biopharmaceutical Excipient Manufacturing Market: Industry Trends and Global Forecasts, 2022-2035

Contact:

Ben Johnson

+1 (415) 800 3415

+44 (122) 391 1091